Read this if you are a business owner or an advisor to business owners.

This article is part three of a three-part series.

With continued uncertainty in the business environment—driven by shifting economic conditions, market volatility, and evolving tax policy—now may be a good time to utilize trust, gift, and estate strategies in the transfer of privately held business interests. Periods of uncertainty can create an opportunity to free up considerable portions of lifetime gift and estate tax exemption amounts through transfers, particularly as uncertainty and increased risk serve to reduce business valuations.

An element to consider is the ability to transfer noncontrolling interests in a business. These interests are potentially subject to discounts for lack of control and lack of marketability. This may further reduce the overall value transferred through a given strategy, potentially offloading a larger percentage of ownership in a business while retaining large portions of the gift and estate lifetime exemption. Part one of this series focused on the discount for lack of control (DLOC) and part two focused on the discount for lack of marketability (DLOM). In part three, we’ll focus on the application of discounts.

Application of discounts

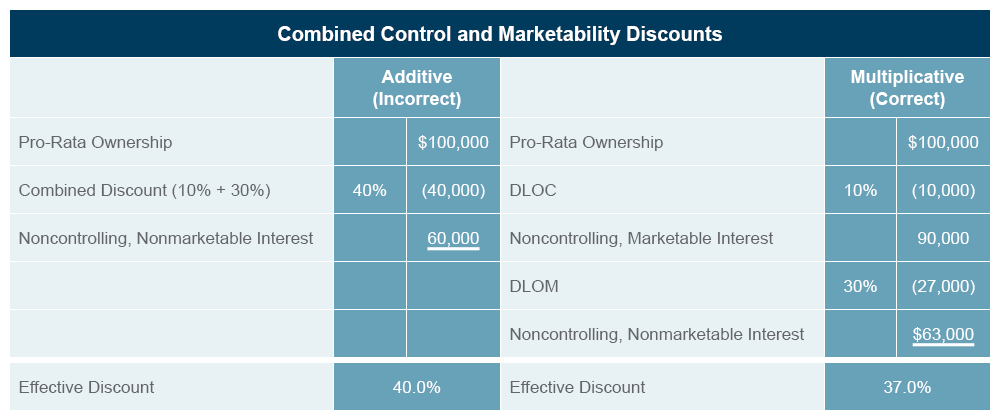

One area that often challenges those unfamiliar with business valuations is the application of the DLOC and DLOM. These discounts are multiplicative, not additive. The combined effect of a 10% DLOC and a 30% DLOM is not an additive result of 40%, rather a multiplicative result of 37% (mathematically, 1 – [(1 – DLOC) x (1 – DLOM)]). Consider the following example:

A business owner has a 10% minority, nonmarketable interest in a business. The equity of the business is worth $1,000,000. Their interest has a pro-rata value of $100,000 (10% of $1,000,000). They retained a qualified valuation analyst, who estimated that a 10% discount for lack of control and a 30% discount for lack of marketability were appropriate for the valuation of the business owner’s interest. The difference in applying these discounts correctly through a multiplicative process and incorrectly through an additive process is demonstrated in the following chart:

It does not matter the order in which a DLOC and a DLOM are applied. Because these discounts are multiplicative, applying either one first will not affect the concluded minority, nonmarketable value.

What this means for business owners

Business owners are knowledgeable of the facts and circumstances surrounding a business interest. They take a close look at what they are buying before they make an offer. Like most owners, they prefer to maintain control and invest in assets that are readily convertible to cash. Therefore, they are generally not willing to pay the pro-rata value for a minority interest in a business that lacks control and marketability. To assess appropriate discounts for lack of control and discounts for lack of marketability, consider resources such as those referred to in part one and part two of this series, then ensure the selected discounts are appropriate based on the factors specific to the company and interest being valued. From there, the application of the DLOC and DLOM is multiplicative, not additive, as noted in the example above.

Given the current environment, using trust, gift, and estate strategies that take advantage of discounts for lack of control and marketability offers the opportunity to transfer a higher percentage of interest in a privately held company at a lower value. This potentially frees up additional amounts of remaining thresholds of the lifetime gift and estate tax exemptions.

Key takeaways

- Watch for market and tax uncertainty that can create transfer opportunities.

- Identify noncontrolling interests that may qualify for valuation discounts.

- Distinguish discounts for lack of control from discounts for lack of marketability.

- Apply the two discounts multiplicatively rather than adding the percentages.

BerryDunn can help

BerryDunn’s credentialed business valuation specialists bring clarity to the complexities of valuation while adhering to strict development and reporting standards. We render an independent, objective opinion of your company’s value in a reporting format tailored to meet your needs. If you have questions about your unique situation, or would like more information, please contact the business valuation consulting team.

Skip to Main Content

Skip to Main Content