Read this if you are considering adding telehealth services, or enhancing your your current telehealth services.

Consumer and provider’s perceptions and adoption of telehealth in the US have been mixed at best. The current COVID-19 pandemic has necessitated and supported broader use of non-face-to-face provider interactions. Payor changes will likely continue post-pandemic, and the communities we serve may expect more virtual care options.

The regulatory changes necessitated by the pandemic provide new flexibility and options to serve our patients remotely and generate revenue. Leveraging this opportunity demands:

- understanding each payor’s requirements,

- educating providers,

- creating revenue cycle processes, and

- ensuring compliance with payor requirements.

Providers need to understand the “flavors” of non-face-to-face visits, the payor requirements, and the significant payment differences. Simple documentation, modifier, and/or claim form omissions can mean the difference between being paid for a face-to-face office visit versus a non-chargeable service. The effort in getting it right today will have immediate benefits that should extend into post-pandemic operations.

The first step is researching and documenting each payor’s requirements. The rules and regulations are not the same for RHCs, FQHCs, Method II billing, and the different provider types such as physical therapists and MDs. Providers need to understand documentation, CPT/HCPC, modifier, place-of-service, video requirements versus audio only, and other nuances. Simplification of each payor’s rules into an easy-to-digest grid creates an invaluable tool for everyone involved. Below is an example of a payor grid:

| Payor |

Sample payor 1 |

Sample payor 2 |

| Video requirement waived? |

Yes |

No |

| Place of service |

02 |

02 for 11 |

| Virtual check-in/brief communication codes |

G2012 or G2010 |

G2012 or telephone E/M codes (G99441-99433) |

| Telehealth service codes |

All codes in CPT Appendix P |

All codes in CPT Appendix P, video required, use office POS |

| Modifier rules |

V3 required for audio only visits |

95 or GT |

| Note |

Use G2012 for triage |

Payor notes that most appropriate level is 99212 or 99213 |

Other questions on payor requirements that may prove worth tracking:

- Will cost shares be waived?

- Is payor reimbursing at face-to-face rates?

- Are telehealth services limited to established patients?

- Are requirements around follow-up appointments bundled or not?

- For organizations with multiple provider types, what claim type is required?

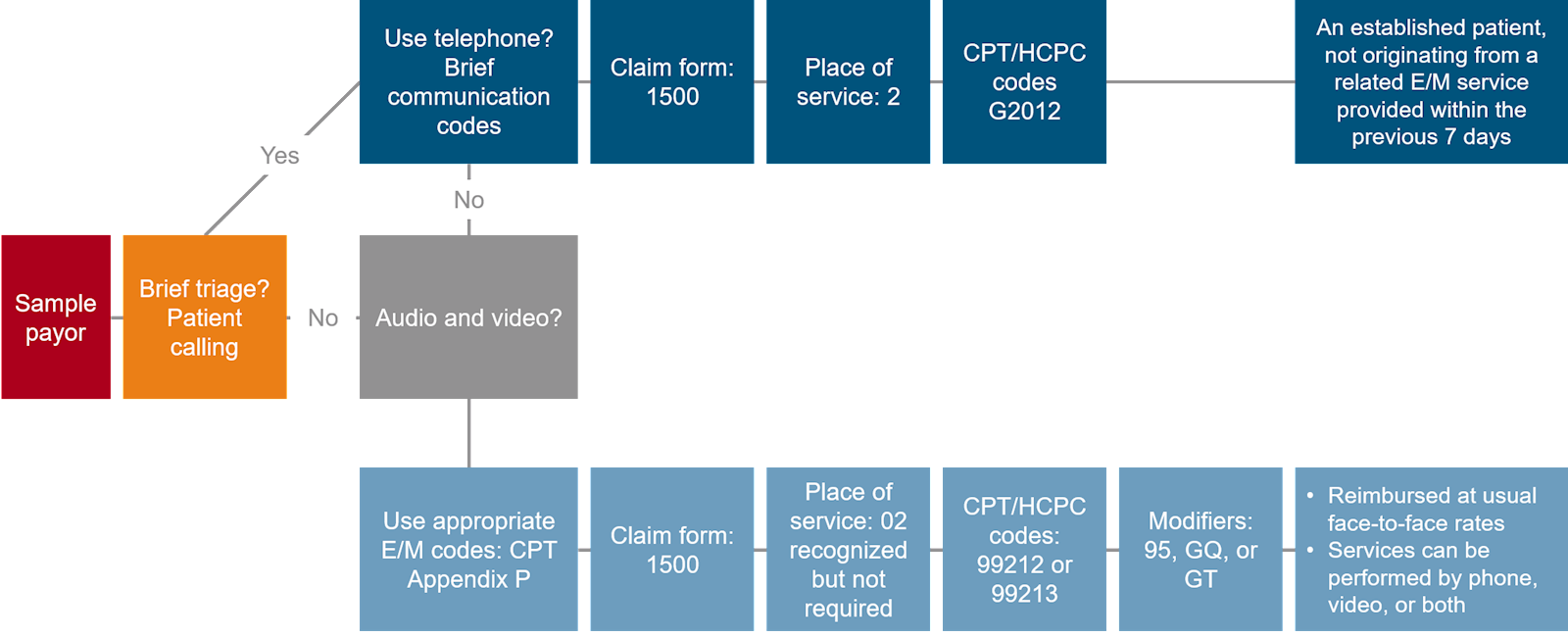

Every member of the revenue cycle must be involved to optimize telehealth services. Do not overlook the importance of registration, IT/system configuration (from a documentation and billing perspective), and physician education. Providers should consider simple flow charts to assist in operationalizing the rules by payor. For example (click to expand):

The government relaxed HIPAA rules allowing providers many more options for telehealth technology (such as using Web-Ex, Skype, Zoom, and other readily available services). These options are of no value if not available and/or adopted by providers and patients. In terms of payment, the lack of a video component is often the difference between billing and being paid at the face-to-face in office rate versus a non-chargeable or minimal payment service. Some payors are allowing and paying audio-only visits at the office rate, which further highlights the need to understand the rules.

Here is an example from Medicare showing the potential payment difference between an audio-only and video-enabled service:

| Code |

Long description |

Medicare fee schedule rate |

| 99442 |

Telephone evaluation and management service; 11-20 minutes of medical discussion. |

$27.82 |

| 99213 |

Office or other outpatient visit for the evaluation and management of an established patient, which requires at least 2 of these 3 key components: an expanded problem focused history, an expanded problem focused examination, and/or medical decision making of low complexity.

Counseling and coordination of care with other physicians, other qualified health care professionals, or agencies are provided consistent with the nature of the problem(s) and the patient's and/or family's needs. Usually, the presenting problem(s) are of low to moderate severity. Typically, 15 minutes are spent face-to-face with the patient and/or family. |

$77.15 |

In this example, the physician time is about 15 minutes with the patient. However, if video were used the payment would be 177 percent more. When you account for the number of physicians in your organization that are providing these visits every day times the payment difference, the delta is substantial. The payment difference is even more significant for other codes and payor rates (and further exacerbated by payers that do not pay for audio-only visits).

There are significant payment difference between the different codes that can be billed for telehealth visits by payor. These are difficult financial times for providers and every dollar counts. BerryDunn is available to help if you have questions around rules, regulations, and/or best practice processes around billing for these services. You can e-mail Denny Roberge or call 603.518.2623 with any questions or for assistance optimizing your telehealth program.

Skip to Main Content

Skip to Main Content